It’s easy to feel overwhelmed by finances, especially when life keeps throwing unexpected expenses your way. We all want a little more breathing room in our bank accounts without giving up everything we love. This guide cuts through the noise to offer 20 practical and relatable Saving Money Tips and budgeting tips that real people can use to start building a stronger financial future right now.

1. Master Your Budget (The Foundation of Saving)

The cornerstone of any successful savings strategy is a clear, functional budget. You cannot effectively save money if you don’t know where your money is currently going. Many people skip this step because they find it intimidating, but modern tools make it easier than ever.

How to Do It: The 50/30/20 Rule

One of the most effective budgeting tips is the 50/30/20 rule, which simplifies spending categories:

- 50% for Needs: Essential fixed expenses like rent/mortgage, groceries, utilities, and debt minimum payments.

- 30% for Wants: Non-essential, discretionary spending like dining out, entertainment, hobbies, and shopping.

- 20% for Savings and Debt Repayment: This portion goes directly into your savings strategy (emergency fund, retirement) and paying down high-interest debt faster.

Example: If your take-home pay is $4,000 per month, allocate $2,000 to needs, $1,200 to wants, and $800 directly to savings/debt.

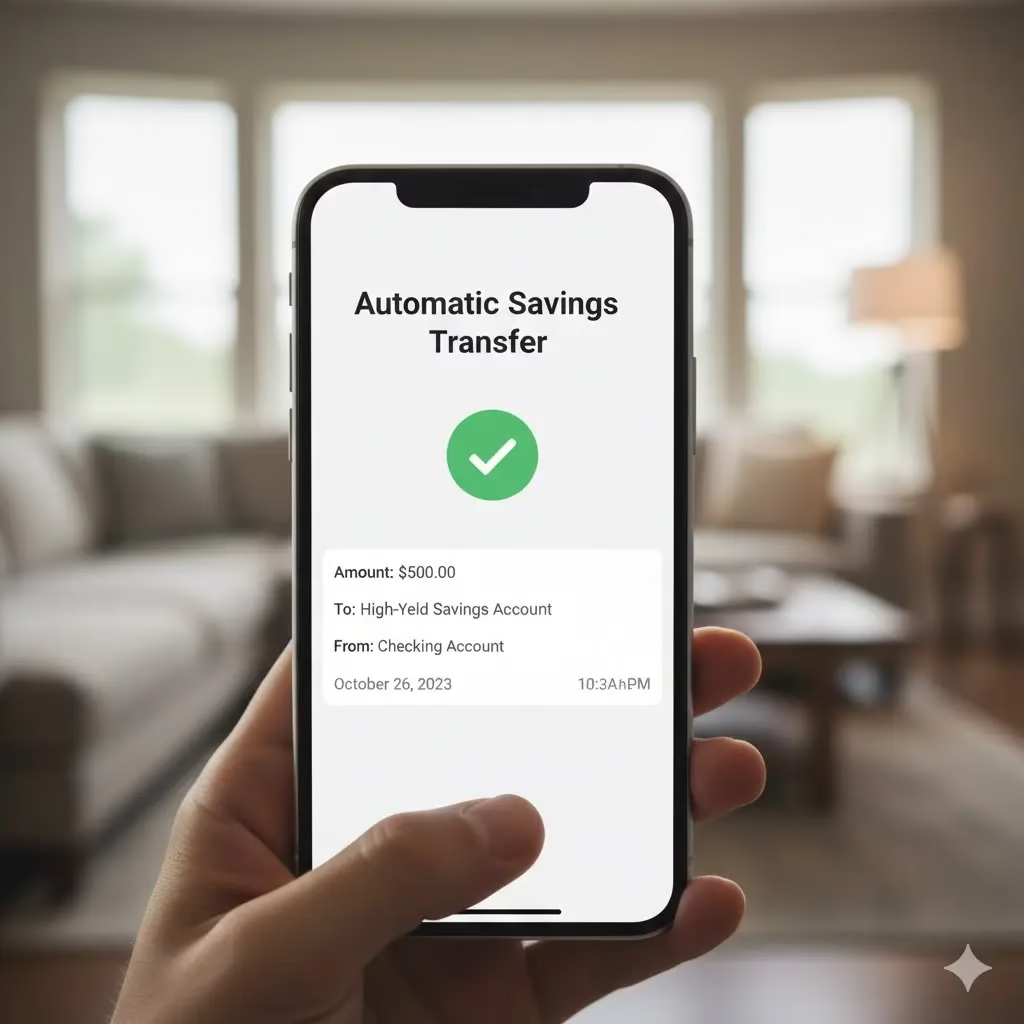

2. Automate Your Savings

This is one of the most powerful money saving techniques because it removes the temptation to spend. If you don’t see the money, you won’t miss it. Saving should be treated as a non-negotiable expense, just like rent.

How to Do It: Set it and Forget it

Contact your bank or use your payroll provider to automatically transfer a fixed percentage or amount of every paycheck into a separate, high-yield savings account the day you get paid. For instance, if you decide your savings strategy includes saving 15% of your income, ensure that 15% is moved before you have a chance to budget it for anything else. This is a game-changer for consistency.

3. Implement the Waiting Period Rule

Impulse buying is a major budget killer. This simple money saving technique gives your rational brain a chance to catch up with your emotional desire to purchase.

How to Do It: The 48-Hour Delay

For any non-essential purchase over a set amount (e.g., $50 or $100), commit to waiting 48 hours before buying it. Put the item in your online cart or write it down. If, after two days, you still feel it’s a necessary or valuable purchase, go ahead. More often than not, the urge will pass, and you’ll save the money.

4. Conduct a Subscription Audit

We often sign up for free trials and then forget to cancel, bleeding small amounts of money every month. This audit can reveal easy wins for your budgeting.

How to Do It: The Annual Review

Once every six months, go through your bank and credit card statements line-by-line. Highlight every recurring charge. Ask yourself two questions for each: Do I actively use this? Can I downgrade or share this with a family member? Cancel or pause anything you haven’t used in the last month or two.

5. Embrace the Home-Cooked Meal

Eating out, even occasionally, significantly impacts your budget. Learning to cook a few simple, cost-effective meals is a core Saving Money Tip.

How to Do It: The 3-Meal Rotation

Plan and master three inexpensive meals that you enjoy and can make in large batches (e.g., lentil soup, chili, or chicken and vegetable stir-fry). Make enough for four servings in one go. You now have dinner for one night and three lunches, drastically cutting down on the cost of takeout lunches and reducing food waste.

6. Negotiate Your Bills

From your internet provider to your car insurance, loyalty is rarely rewarded. Being proactive and calling your service providers is a key money saving technique.

How to Do It: Call and Compare

Call your cable or internet provider and mention that you are considering switching to a competitor. Ask if they can offer you a retention rate or a promotional package. Do this for every service, including mobile phone plans and insurance. You can often save $10 to $50 per month on each call.

7. The Power of “No Spend” Days

This saving money tip focuses on controlling discretionary spending by periodically eliminating it entirely. It’s an effective way to reset spending habits.

How to Do It: Challenge Yourself

Start with one “No Spend Day” per week where you commit to spending zero dollars. This means no coffee shop visits, no takeout, no impulse purchases, and using what you already have. Once successful, consider challenging yourself to a “No Spend Weekend” once a month.

8. Start an Emergency Fund

An emergency fund is the shield for your savings strategy. Without one, any unexpected expense (like a car repair or medical bill) will immediately derail your budget and force you into debt.

How to Do It: The $1,000 Milestone

Focus relentlessly on saving a starter amount of $1,000. This is enough to handle most minor emergencies. Once you hit the $1,000 target, pivot your savings strategy to a larger goal: 3-6 months’ worth of living expenses. This money should be kept in a separate, easily accessible (but not too easy) high-yield savings account.

9. Review Your Tax Withholdings

Getting a huge tax refund every year isn’t necessarily a good sign; it means you gave the government an interest-free loan throughout the year. Adjusting your withholdings is a simple money saving technique to give you more take-home pay immediately.

How to Do It: Consult an Expert

Speak with a financial advisor or use an online calculator to determine the correct number of allowances to claim on your W-4 form. The goal is to adjust your withholdings so that your tax liability is close to zero, putting more money in your monthly paychecks that you can then funnel into your savings strategy.

10. Pay Off High-Interest Debt First (The Debt Avalanche)

High-interest debt, like credit cards, acts like a negative savings account, costing you money every day. Aggressively paying this down is the most profitable saving money tip you can follow.

How to Do It: Focus on Interest Rate

List all your debts from highest interest rate to lowest. Commit all extra funds (beyond minimum payments) to the debt with the highest rate. Once that debt is paid off, take the money you were paying on it and apply it to the next highest-rate debt. This is called the Debt Avalanche method, and it saves the most money on interest over time.

11. Use the Library, Not the Bookstore

The cost of books, DVDs, and streaming rentals adds up quickly. Your local public library is a vast, free resource for entertainment and learning.

How to Do It: Get Your Card

Obtain a library card and use their services for books, audiobooks, movies, and magazines. Many libraries also offer free access to online courses and digital magazines, which is a fantastic budgeting tip for personal development without the cost.

12. Reduce Energy Vampires

Even when turned off, many electronics (TVs, chargers, coffee makers) continue to draw power, known as ‘phantom load’ or ‘energy vampires’.

How to Do It: Plug Into Strips

Plug all related electronics (like your TV, gaming console, and sound system) into a single power strip. When you are done using them, flip the switch on the power strip off. This simple action can save a noticeable amount on your monthly utility bill, an easy money saving technique.

13. Drive Smart and Maintain Your Vehicle

The way you drive and care for your car directly affects your gas and maintenance costs.

How to Do It: Consolidate Trips and Check Tires

Group errands together to avoid multiple cold starts. More importantly, check your tire pressure monthly. Under-inflated tires decrease gas mileage and wear out faster, costing you more money. Proper maintenance, like timely oil changes, prevents costly, long-term repairs—a smart budgeting tip for vehicle ownership.

14. Embrace Generic and Store Brands

In many cases, the store brand or generic version of a product (especially for staples like medicine, cleaning supplies, and some food items) is virtually identical to the brand-name product, often made in the same factory, but at a significantly lower price.

How to Do It: Start Small

Try swapping three brand-name items in your grocery cart for the generic equivalent on your next shopping trip. If you don’t notice a difference, make the switch permanent. This small saving money tip can easily save you $20-$40 per trip.

15. The Envelope System (For Cash Spenders)

This classic budgeting method is perfect for people who overspend when using a debit or credit card. It provides a visual and physical barrier to spending.

How to Do It: Cash Only Categories

At the start of the month, withdraw the exact amount of cash allocated for your most problematic categories (e.g., dining out, entertainment, and miscellaneous shopping). Place the cash in separate, labeled envelopes. When the cash in an envelope is gone, the spending for that category is over until the next month.

16. Host Potlucks Instead of Going Out

Socializing is important, but a night out can cost upwards of $50 per person. Changing how you socialize is a simple saving money tip.

How to Do It: Make it Collaborative

Instead of suggesting a restaurant, invite friends over for a potluck dinner. Assign categories (one person brings a main dish, another a side, another a dessert, and another drinks). Everyone gets to eat, socialize, and you all save money.

17. Use the “Found Money” Rule

When you receive money you weren’t counting on (a work bonus, a small refund, a gift), it’s easy to treat it as “fun money” and spend it carelessly.

How to Do It: Allocate Unexpected Funds

Commit to putting 50-100% of any unexpected income directly toward your established savings strategy (either the emergency fund or paying down high-interest debt). If you get a $500 work bonus, putting $400 into savings means you get a huge boost while still leaving yourself $100 for a treat.

18. Refinance High-Interest Loans

[Image of a graphic showing a ‘Before’ loan rate at 18% and an ‘After’ rate at 7% on a document.)

If you have debt like a mortgage, student loans, or personal loans, exploring refinancing options can be a highly effective, long-term money saving technique.

How to Do It: Shop Around

Check your credit score and then approach a few different financial institutions to see if you qualify for a lower interest rate on your existing debt. Even a small drop in the interest rate can save thousands of dollars over the life of the loan and free up significant cash flow for your monthly budgeting.

19. Check Unit Pricing at the Grocery Store

The large price on the tag is not always the best indicator of value. The true saving money tip for groceries is using the unit price.11

How to Do It: Read the Fine Print

Every price tag in the grocery store should list the price per unit (e.g., $0.15 per ounce or $0.50 per sheet). Train yourself to compare the unit price between similar items and different sizes. The largest size is often, but not always, the best value.

20. Embrace the Savings Goal Mindset

The most effective savings strategy is one that is motivated by a clear, exciting goal. Saving for “just in case” is less motivating than saving for a dream vacation or a down payment on a home.

How to Do It: Make Goals Specific (SMART)

Give your savings goals a name, an amount, and a deadline. Instead of “Save more money,” write “Save $5,000 for a trip to Portugal by December 2026.” This gives your automatic transfers and budgeting sacrifices purpose, making the process sustainable and rewarding.

Frequently Asked Questions (FAQ)

Q: What is the single best money saving technique I can start today?

A: The most impactful technique is automating your savings. By setting up an automatic transfer from your checking account to a savings account on payday, you ensure that saving happens before you have a chance to spend the money. This makes saving consistent and non-optional, instantly boosting your savings strategy.

Q: How often should I check my budget?

A: You should track your spending daily or every few days to ensure you are sticking to your plan, but you should perform a comprehensive review of your budget at least once a week. A monthly budget review is also essential to compare actual spending against your planned spending and make adjustments for the coming month, following a key budgeting tip.

Q: How much money should I aim to save from my paycheck?

A: A widely recommended benchmark is the 50/30/20 rule, which suggests putting 20% of your after-tax income toward savings and debt repayment.12 If 20% is not feasible right now, start with 5% or 10% and incrementally increase the percentage every few months. The key is to be consistent, as consistency is a crucial Saving Money Tip.

Q: Is it better to save or pay off debt?

A: In most cases, you should first save a small starter emergency fund (e.g., $1,000). After that, the savings strategy priority should be paying off high-interest debt (like credit cards with rates over 10-15%) because the interest you save typically far outweighs the interest you would earn in a typical savings account. Once high-interest debt is gone, you can shift focus entirely to building a full emergency fund and other savings goals.

References

- USA – Tips for budgeting to meet your financial goals

- Consumer – Making a Budget

- Trust Point – 6 Key Benefits of a Financial Plan

Recent Posts